Hello. Your user experience on our site might be different because you are on Internet Explorer, switch to Chrome or Safari for a better experience.

Bank of Canada Cuts Policy Interest Rate Again: What This Means for Homeowners and the Economy

July 24, 2024

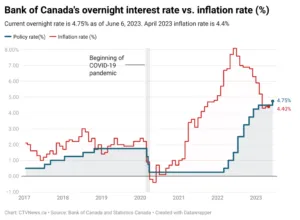

In a significant move to manage inflation and bolster economic growth, the Bank of Canada has once again reduced its policy interest rate. This latest cut of 25 basis points brings the overnight rate down to 4.5%, a level not seen since June 2023. This follows a previous reduction from 5% to 4.75%—the first cut in over four years.

Bank of Canada Governor Tiff Macklem has highlighted key economic indicators that led to this decision, including slack in the labor market, excess supply in the economy, and a continuing drop in inflation. “We are increasingly confident that the ingredients to bring inflation back to target are in place,” Macklem said (CTV News).

Since the Bank of Canada started raising rates in March 2022, inflation has dropped significantly from a peak of 8.1% in June 2022 to 2.7% in June 2024. While a further moderation in inflation is anticipated, Macklem cautioned that progress may be uneven over the next year.

Macklem has hinted at the possibility of additional rate cuts if inflation continues to ease. “If inflation continues to ease broadly in line with our forecast, it is reasonable to expect further cuts in our policy interest rate,” he explained. The timing and extent of these cuts will depend on forthcoming economic data.

Economists and major banks forecast up to four more rate cuts by the end of 2024. The pace of these reductions may be influenced by actions taken by the Bank of England and the U.S. Federal Reserve. Notably, the Bank of Canada was the first among the Group of Seven central banks to implement a rate cut since the pandemic began (CTV News).

After stagnating in late 2023, Canada’s GDP saw a growth of approximately 1.75% in Q1 2024, driven by robust population growth. The central bank projects ongoing economic expansion through the latter half of 2024, supported by easing interest rates and increasing confidence among households and businesses. GDP growth is expected to reach around 2.1% in 2025 and 2.4% in 2026 (CTV News).

Core inflation is anticipated to ease to about 2.5% in the second half of 2024. However, the path to the target inflation rate of 2% may be uneven, with CPI inflation likely rising slightly in the first half of 2025 before stabilizing at 2% later in the year (CTV News).

Several risks could impact the inflation outlook, including global geopolitical events such as trade disruptions from conflicts in the Middle East and Ukraine. These situations could affect commodity prices and supply chains, potentially delaying progress toward the inflation target (CTV News).

Another concern is the persistently high shelter costs, driven by population growth and housing shortages. These high prices are expected to continue exerting upward pressure on inflation. The Bank of Canada’s recent report highlights the significant impact of immigration on the housing market, particularly in rental sectors, which has contributed to higher shelter costs (CTV News).

The Bank of Canada’s latest report emphasizes the considerable effect of immigration on the Canadian economy and housing market. Over the past two years, Canada’s population has increased by 6%, largely due to the influx of immigrants. This surge has boosted consumer spending and enhanced the economy’s potential for non-inflationary growth by an estimated 2.5%. However, many newcomers have faced challenges finding employment, which has somewhat limited their impact on the labor market. The population boom has notably increased demand in the rental market, leading to higher rents and home prices (CTV News).

For homeowners, particularly those with variable-rate mortgages, the recent interest rate cuts provide some much-needed relief. According to Rates.ca, each 25-basis point reduction translates to about $15 less per $100,000 of mortgage in monthly payments. This adjustment offers welcome breathing room for those with floating variable-rate mortgages (CTV News).

However, the broader housing market might not see a significant uptick in activity from these cuts alone. Many potential buyers remain cautious and are waiting for further reductions. Experts suggest that a substantial increase in sales activity would likely require an additional cut of 25 to 50 basis points.

Despite this, the consecutive rate reductions signal positive momentum for the economy. As mortgage qualification thresholds decrease, sidelined buyers may feel more confident about re-entering the housing market. “A second cut to the overnight lending rate indicates that the economy is moving in the right direction,” noted Karen Yolevski, COO of Royal LePage Real Estate Services Ltd.

The Bank of Canada’s recent interest rate cuts are designed to support economic growth while managing inflation. Although the journey to the 2% inflation target may be uneven, these measures provide relief to homeowners and suggest a positive economic trajectory. As conditions evolve, additional rate cuts may be on the horizon, potentially creating new opportunities for buyers and sellers in the housing market.

Cedarbrook is the premier choice for master-planned living in Chilliwack. Contact us at (604) 793-8578 or fill our Contact Form to schedule a tour and discover the difference for yourself!

Come experience the community for yourself.